U.S. Treasury Evaluates Digital Identity Integration in DeFi to Strengthen Oversight and Mitigate Illicit Financial Activities. As decentralized finance (DeFi) continues to expand and reshape the global financial landscape, regulators are seeking new ways to ensure compliance without stifling innovation. The U.S. Treasury is now exploring how digital identity technologies can be integrated into blockchain protocols to combat illicit activities

The United States Department of the Treasury has initiated a public consultation process aimed at exploring how digital identity technologies, smart contract integrations, and advanced compliance frameworks can be leveraged to reduce illicit financial activities within decentralized finance (DeFi) ecosystems. This initiative reflects a broader regulatory shift toward embedding security, transparency, and accountability mechanisms directly into the infrastructure of blockchain-based financial systems, particularly as these technologies become more embedded in global capital markets.

The request for public comments—announced in August 2025—derives its authority from the recently enacted Guidance and National Innovation Uniformity for Stablecoins Act (GENIUS Act), which came into force in July. The GENIUS Act establishes a formal regulatory framework for U.S.-based payment stablecoin issuers, mandating comprehensive compliance standards that align with existing anti-money laundering (AML) and counter-terrorism financing (CTF) laws. Importantly, the Act also calls on federal agencies to examine the role that emerging technologies—including APIs, artificial intelligence (AI), distributed ledgers, and digital identity verification systems—can play in improving oversight and reducing systemic risk.

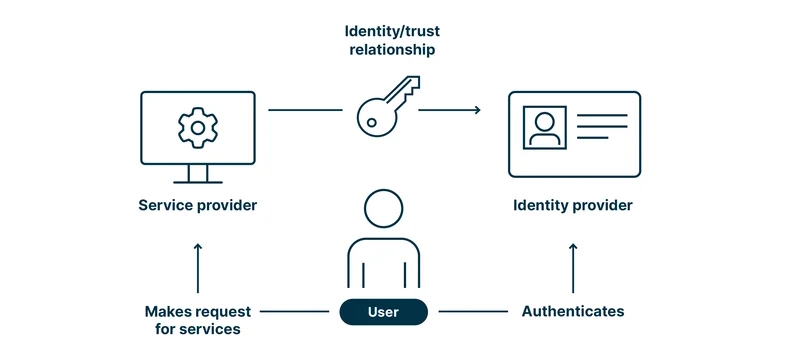

One of the most significant technological proposals being evaluated is the potential for on-chain digital identity verification, where decentralized protocols would incorporate identity credentials directly into smart contract logic. Under this model, user identities would be verified through cryptographically secure credentials—such as government-issued digital IDs, zero-knowledge proofs, biometric data, or portable verifiable credentials—before any transaction is executed. This would effectively integrate Know Your Customer (KYC) and AML checks into the base layer of DeFi operations, eliminating the need for third-party intermediaries in many instances while maintaining regulatory compliance.

This model introduces a paradigm shift in how financial compliance could be enforced in decentralized environments, where no central authority exists to vet participants. For example, a DeFi lending protocol could refuse to execute smart contract functions if the interacting wallet address does not provide a valid, verifiable identity token issued by a trusted identity provider. These verifications could be performed using decentralized identity (DID) frameworks, which are compliant with standards from organizations such as the W3C and enable users to control their personal data while still satisfying compliance requirements.

The Treasury has highlighted the potential for digital identity solutions to significantly reduce compliance costs for both centralized and decentralized financial institutions. By automating identity verification and transaction screening, these technologies could streamline onboarding, reduce false positives in transaction monitoring systems, and enable near real-time due diligence. Moreover, they may offer stronger privacy guarantees than traditional identity systems, particularly when paired with advanced cryptographic techniques such as homomorphic encryption or zero-knowledge proofs, which allow identity verification without revealing underlying personal information.

However, the Department also acknowledged a number of technical and ethical challenges. Key concerns include the risk of mass surveillance, potential misuse of biometric data, the fragmentation of identity standards across jurisdictions, and the challenge of enforcing compliance across open-source protocols that can be forked or cloned. Moreover, questions remain about the governance and trustworthiness of digital identity issuers, especially in cross-border contexts where geopolitical and legal frameworks diverge. The Treasury is therefore soliciting feedback on how to ensure interoperability, user privacy, and technological neutrality in any future regulatory framework.

The public consultation period is open until October 17, 2025, and feedback is being accepted from a wide range of stakeholders, including developers, financial institutions, civil society organizations, and cybersecurity experts. Following the conclusion of the consultation, the Treasury will prepare a comprehensive report for Congress, which may include legislative recommendations, proposed rulemakings, or implementation guidelines for future compliance technologies in the digital asset space.

This initiative comes amid heightened scrutiny of stablecoins and DeFi protocols, which have rapidly grown in volume and complexity, attracting both legitimate financial activity and illicit uses. According to the Treasury, stablecoins—cryptocurrencies pegged to fiat currencies—pose unique regulatory challenges due to their potential to serve as both payment mechanisms and interest-bearing financial instruments. Their programmable nature enables them to be integrated into yield-generating DeFi protocols, liquidity pools, and lending platforms, raising concerns about their use in circumventing traditional banking regulations.

In a related development, several major U.S. banking associations, led by the Bank Policy Institute (BPI), have raised alarms about a perceived loophole in the GENIUS Act that could allow stablecoin issuers to bypass restrictions on interest payments. In a letter to Congress dated August 19, 2025, the BPI warned that issuers might collaborate with affiliated exchanges or offshore entities to offer yield-bearing stablecoins, undermining the law’s objective to draw clear lines between stablecoins used as cash equivalents and those functioning as investment products.

The BPI argued that such activities could distort the competitive landscape by encouraging a large-scale migration of deposits away from traditional banks—potentially up to $6.6 trillion, according to their estimates—thus weakening the banking sector’s ability to finance business lending and economic growth. The Institute has called for amendments to the GENIUS Act that would explicitly prohibit any indirect arrangements aimed at providing returns on stablecoin holdings, regardless of the legal structure used.

Overall, the Treasury’s move to explore technical compliance solutions within DeFi protocols reflects a growing recognition that purely reactive or enforcement-based approaches are insufficient in the face of decentralized, code-based financial systems. Instead, embedding regulatory logic directly into financial software—sometimes referred to as “RegTech for DeFi”—may offer a more scalable, transparent, and innovation-compatible path forward. However, its success will ultimately depend on the ability to balance regulatory objectives with core Web3 principles such as privacy, autonomy, and decentralization.