As global regulators grapple with the challenges posed by decentralized finance, the Bank for International Settlements (BIS) has introduced a bold proposal to classify digital assets like Bitcoin based on their transaction histories. The plan envisions a blockchain-based scoring system that could redefine the legal and financial status of cryptocurrencies

BIS Proposes Blockchain-Based Scoring System to Classify Bitcoin as Legal or Illicit: A New Regulatory Paradigm

In a move that could significantly reshape the global cryptocurrency landscape, the Bank for International Settlements (BIS) has proposed a blockchain-integrated scoring mechanism aimed at categorizing digital assets—such as Bitcoin and stablecoins—as either “legal” or “illegal” based on their transactional history. Presented in a recent bulletin, the initiative introduces a framework that combines blockchain’s inherent transparency with regulatory compliance measures to assess the risk level associated with each unit of digital currency. At its core, the system aims to address a growing challenge for regulators and financial institutions: how to maintain financial integrity and prevent illicit activity in decentralized, pseudonymous financial ecosystems.

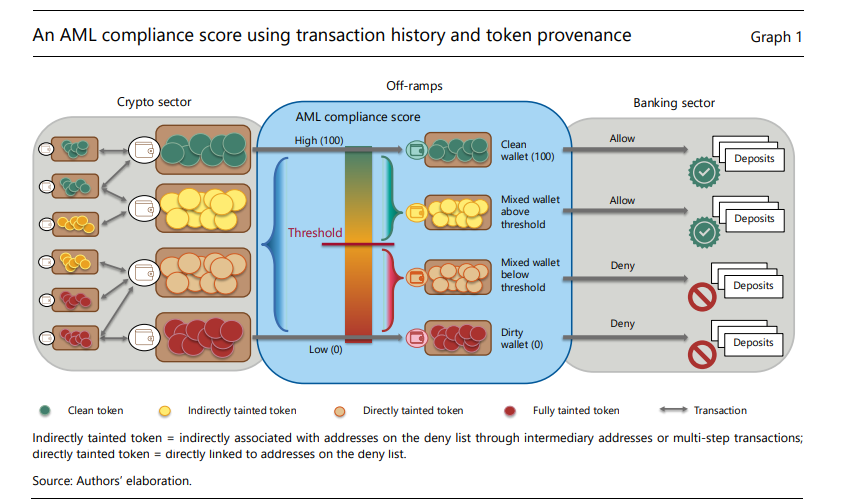

The central concept involves assigning a score to individual units of cryptocurrency, ranging from 0 to 100, reflecting their association—or lack thereof—with illicit activities. This score would be determined through the analysis of transaction histories on public blockchains, leveraging tools commonly used in forensic blockchain analytics. These tools, often employed by companies such as Chainalysis, Elliptic, or CipherTrace, trace the provenance of digital assets, map transaction flows, identify wallet clusters, and flag entities connected to known illicit activities such as darknet markets, ransomware payments, mixers (also known as tumblers), and wallets tied to sanctioned individuals or organizations.

Assets with a clean transaction trail, ideally stemming from wallets that have undergone Know Your Customer (KYC) verification or are linked to regulated entities, would be rated near the top of the scale. These assets would be deemed safe for use within the traditional financial system, facilitating their conversion into fiat currencies or their use in regulated crypto services. Conversely, units that have passed through addresses associated with criminal activity, high-risk jurisdictions, or unregulated services would receive low scores. These “tainted” coins could be effectively blacklisted, severely limiting their utility in legitimate markets.

The BIS proposal extends far beyond mere scoring. It advocates for the institutionalization of this mechanism across exchanges, banks, custodial services, and stablecoin issuers. Under such a framework, any entity operating within the regulated financial environment would be obliged to check an asset’s score before processing a transaction involving it. This would effectively introduce a layer of programmable compliance within the crypto ecosystem, where the permissionless nature of blockchain transactions is tempered by a gatekeeping mechanism at the point of interaction with fiat systems.

This approach raises profound implications for the principle of self-custody, a foundational ethos of the cryptocurrency movement. While users could continue to hold their private keys and move assets within the blockchain ecosystem, their ability to interface with the broader economy—such as converting crypto to fiat, accessing decentralized finance (DeFi) protocols that integrate with regulated entities, or using crypto for real-world payments—would be constrained by the scoring system. Anonymously received coins, even if acquired legally, could become stranded if they are flagged as high-risk, reducing their liquidity and usability.

Furthermore, the proposal is likely to intensify the already growing regulatory push for stringent KYC and anti-money laundering (AML) compliance in the crypto sector. Under this system, the origin and flow of every digital asset would matter, not just at the point of entry or exit from exchanges, but at every step of its lifecycle. Transfers between self-hosted wallets, previously a grey area in regulation, could also come under scrutiny if they involve high-risk coins. Users and businesses may be forced to rely on third-party analytics providers to verify the cleanliness of assets before accepting them, leading to increased costs, slower transactions, and a potential dependency on centralized services for risk assessment.

From a technological standpoint, implementing such a scoring system would require close cooperation between blockchain analytics firms, financial institutions, and regulatory bodies. It would also necessitate the development of global standards for scoring criteria, risk thresholds, and dispute resolution mechanisms in cases of false positives or contested histories. Machine learning models could be employed to automate risk classification, but transparency in how these models are trained and applied would be crucial to maintaining fairness and avoiding overreach.

Proponents argue that such a system could significantly enhance the fight against money laundering, terrorist financing, and cybercrime, especially in an era where cryptocurrencies are increasingly used in sophisticated cross-border schemes. Traditional AML approaches, which rely heavily on intermediaries and manual reporting, are less effective in decentralized environments where transactions can occur anonymously and across borders in real time. A scoring system that uses blockchain’s own auditability could offer regulators a more scalable and proactive tool for enforcing financial integrity.

However, critics warn that this model introduces the risk of pervasive financial surveillance and the erosion of user privacy. If every coin is continuously monitored and graded, users could be tracked and profiled based on the transactional history of the assets they hold—even if they themselves have done nothing wrong. There are also concerns about centralization: who controls the scoring algorithms, how biases are avoided, and whether appeals or reversals are possible for coins wrongly labeled as tainted. This raises questions about due process, fairness, and the potential weaponization of such tools for political or economic ends.

Ultimately, the BIS proposal represents a major shift in how the global financial system may seek to govern the rapidly evolving world of digital assets. It reflects an acknowledgment that traditional regulatory models are struggling to adapt to decentralized finance, and that new, data-driven approaches are necessary to uphold legal and ethical standards in the digital age. If implemented, the scoring system could become a cornerstone of future crypto regulation—ushering in a regime where digital asset sovereignty comes paired with algorithmic accountability, and where the line between decentralization and compliance becomes increasingly complex to navigate.